In collaboration between TechTable and Vita Vera Ventures, we are pleased to share an updated 2023 Restaurant Tech Ecosystem map.

We all saw that the pandemic brought a wave of experimentation in the restaurant tech space, but we also know that tech-driven change is not always linear.

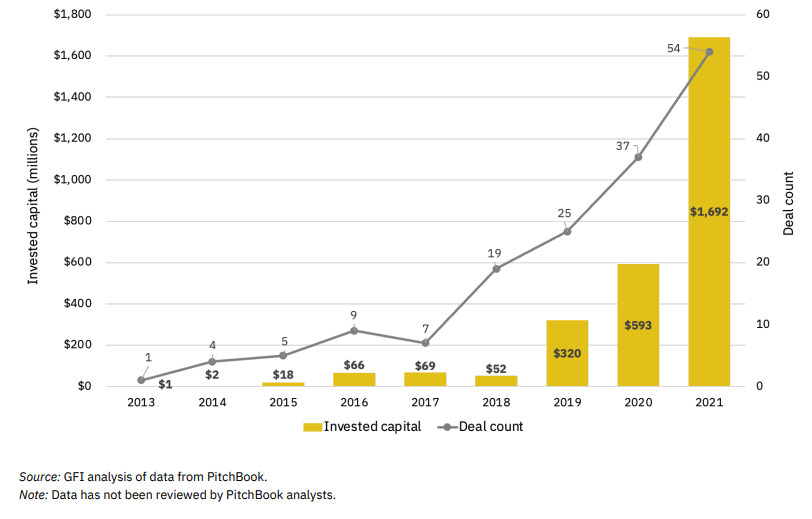

In early 2022, we made bold predictions about the restaurant tech environment in 2023, as we anticipated numerous acquihires ahead (acquisitions primarily driven by tech talent vs strategic tech value). This was due to the tight tech labor market (at the time) and the increasingly challenging funding and interest rate conditions.

However, with the recent wave of macro tech layoffs, the tech labor market is no longer tight, and we believe more restaurant tech companies may be forced to shut down rather than finding a soft landing through acquisition. We’ve already seen a strong reset on requirements for capital efficiency and valuations of startups in the sector. This macro shift may create potential for rollup opportunities, but many early-stage assets across the sector are overfunded single-point solutions and still subscale.

This is ironic as the need for tech-driven solutions has never been stronger, but companies without the right growth metrics will likely struggle to survive. The inflationary environment is also forcing harder decisions for operators, which may further dampen their willingness to engage with new solutions.

With that in mind, we are pleased to share our 2023 Restaurant Tech Ecosystem, which serves as a current heat map of the broader ecosystem within the US (and is clearly not exhaustive).

Click here to enlarge/download image of map. Click here for downloadable PDF.

The Journey from Point Solutions to Comprehensive Tech Stacks

While single-point solutions for things like online ordering, loyalty programs, and delivery were popular during the pandemic, we have reached a moment now with perhaps too many point solutions in the market.

Tech stacks that require too many logins are now in fact creating a cognitive burden for employees, rather than the intended promise of efficiency and ease of use. As a result, operators are beginning to seek integrated systems and smaller tech stacks that can do more. (See commentary in the previous section about rollup opportunities!)

Restaurant tech advisor David Drinan succinctly identifies the near-term priority for most operators: “The restaurant industry is thirsty for technology innovation that will deliver high margin, incremental revenue.”

On the operational side, managers are still struggling with certain areas such as scheduling and inventory management. These tasks can be time-consuming, especially for independent restaurant owners who have limited resources. As a result, we have seen a growth category of solutions that can automate these functions and provide real-time data to help operators make informed decisions.

Help *Still* Wanted

The labor shortage in the restaurant industry has been a major challenge for operators in recent years, and labor optimization is still at the top of every operator’s mind. The pandemic caused many workers to permanently leave the hospitality industry, leaving restaurants short-staffed.

According to the National Restaurant Association, almost two-thirds of US restaurant operators say they do not have enough employees to support existing demand. Instead of replacing this lost workforce, many operators are turning to tech to automate more functions and reduce the need for human labor.

From digital menus and ordering kiosks to automated kitchen equipment, there are many ways that technology can help restaurants operate more efficiently with fewer employees. By automating basic tasks such as taking orders and processing payments, operators can free up their staff to focus on more complex tasks that require human expertise, such as customer service and food preparation.

Another trend the restaurant industry is grappling with is the changing expectations of younger workers when it comes to the employer/employee relationship. With more emphasis on work-life balance, career development, and job satisfaction, younger workers are looking for more than just a paycheck.

To meet these expectations, operators are looking for workforce management solutions that can help to improve engagement, development, and rewards for their employees. This includes tools for tracking and managing schedules, as well as innovative solutions for tip outs and other compensation mechanisms. By investing in these solutions, operators can not only attract and retain top talent but also improve the overall efficiency and productivity of their workforce.

Finally, it is worth noting that basic scheduling and labor management tools can have a significant impact on profitability by reducing labor costs and improving operational efficiency. By automating scheduling and timekeeping, for example, restaurants can reduce the likelihood of overstaffing or understaffing, which can be costly in terms of wasted labor or lost sales opportunities.

In the end, the ability to leverage technology to optimize labor is critical for restaurants to remain competitive in a challenging operating environment. While kiosks and text ordering have shown promise in the QSR space, there are many other opportunities for technology to make a positive impact on the industry as a whole.

Ghost Kitchens: It’s Even More Complicated

In our 2021 restaurant tech retrospective, we had a lot to say about this growing subsector, including the challenges for success (a.k.a. profitability) within the confines of a ghost kitchen business model.

Now, as the concept of virtual and ghost kitchens continues to evolve even further, it’s important for operators to understand the complexities involved and navigate these challenges to build successful ghost kitchen operations.

One major obstacle has been the potential for tension between virtual brands and existing businesses, where adding virtual brands can lead to direct competition with their own existing businesses. Finding the right tech and operational partner to balance between these two is key.

Additionally, ensuring food safety and maintaining quality standards across multiple brands can be a challenge. Many of the generic virtual brands have lacked distinct value or clear taste standards, leading to underwhelming food quality issues and removal from the major third-party delivery platforms.

Last Mile Magic

Making the economics work for restaurant delivery is a growing priority for the industry. This includes better interoperability between POS/Kitchen systems and delivery providers, better routing and batching systems, localized kitchens, and of course even the mode of transportation for delivery.

We are tracking over 20 companies in the North American unattended last mile category, but it is still early days with most (all?) of the solutions operating in limited geographies and customer trials. So we have left this slice off the infographic for 2023, but don’t forget to keep your eyes on the sky, as we’ve seen recent growth of backyard drone delivery companies which are proving to be faster and better for the environment (if they can outweigh the noise and regulatory concerns).

GenAI on the Menu

Tech entrepreneurs have long dreamed of personalized food recommendations, but few have succeeded in creating true personalization beyond dietary concerns, allergens, or ingredient likes/dislikes.

However, we have now reached a unique moment where new technologies like ChatGPT will be able to create meaningful and personalized interactions with guests. This has always been the premise of a variety of AI-driven restaurant tech startups, but the ability to leverage the underlying data to engage and interact with guests in a truly personal and conversational manner is game-changing.

By using data from previous orders and interactions alone, ChatGPT can help to create a more tailored experience for guests, from recommending menu items to offering personalized promotions. ChatGPT can become a critical part of a restaurant’s marketing team by creating content, with the ability to easily translate to different languages as well. This could give operators a crucial competitive advantage as consumers demand more personalized experiences. We have only begun to see the capabilities of ChatGPT with free templates being offered to restaurant operators already.

Moreover, conversational AI like ChatGPT can also be a valuable tool for restaurant operators seeking to understand their own operating metrics. By integrating ChatGPT into their tech stack, operators can ask natural language questions and receive real-time responses, empowering them to make informed decisions about their operations.

Emerging Restaurant Tech Concepts to Watch

- Chat/AI across marketing and operations

- Tech-enabled employee support and training (for example, personalized perks, tip-out options, or language choices)

- AI for scheduling to free up managers

- Dynamic pricing

- Reusable containers + tech-driven circular economy for foodservice

Looking ahead – As always, we welcome your thoughts and reactions, and look forward to continuing to follow this sector together in the coming years. Reach out to us: Brita@vitavc.com and hello@techtablesummit.com.