Welcome to the Spoon Plus Weekly Intelligence Brief. Each week I’ll dissect trends that are unfolding in the world of food tech.

We’ve read a lot over the past two months about the loss of restaurants. Some prognosticators suggest that up to 75% of independent restaurants could permanently disappear.

While the pandemic’s impact on restaurants will continue to be massive and will undoubtedly reshape that industry’s landscape for years to come, another food-related market – appliances and housewares – could also see a dramatic impact in a much different form.

First, the good news. Since quarantines have started in the US, the home appliance market has seen a surge in demand as consumers have shifted to staying and home and eating a much larger number of their meals at home.

Download Report

Did you know you can download a PDF of this report? Just click the download button and you’re good to go.

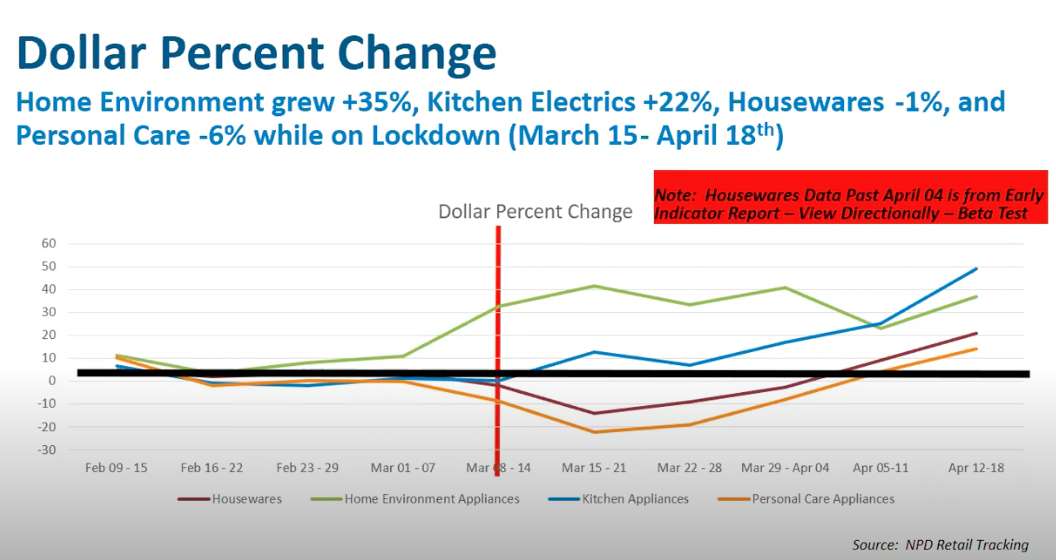

This graphic from NPD’s Joe Derochowski shows how overall kitchen electrics have seen a bump in absolute dollars spent as consumers buy countertop appliances to help them cook at home. Total dollar percentage change for kitchen electrics was up 22% during lockdown.

Figure 1: Percentage Growth of Home Products March 15th-April 18th (NPD Data)

But while a near-term jump in consumer purchases of countertop cooking appliances is no doubt good for the bottom line for some of these companies, the untold story is COVID-19 no doubt set back the same industry from a product roadmap perspective.

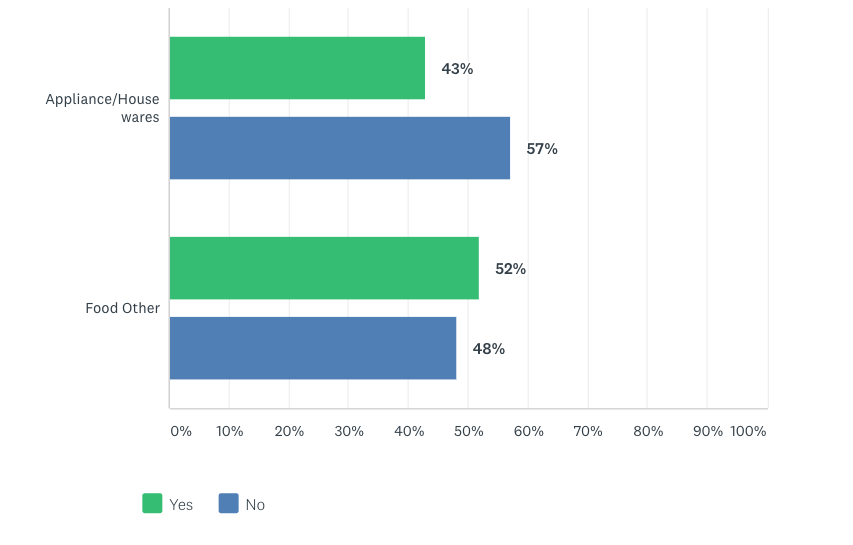

At least that’s my belief after looking at data from our COVID-19 impact survey of food and kitchen industry professionals (see the full report here) conducted in late April. I cut a slice of the data from the survey, which had 377 respondents across the food and related industries, to look at how those within the home appliance and housewares market responded.

As you’ll see from this chart, the appliance/houseware business wasn’t immune to the pandemic’s impact, with 43% indicating their company had to lay off or furlough employees (compared to 52% of the broader food industry).

Figure 2: Have you had to lay off or furlough employees due to COVID-19?

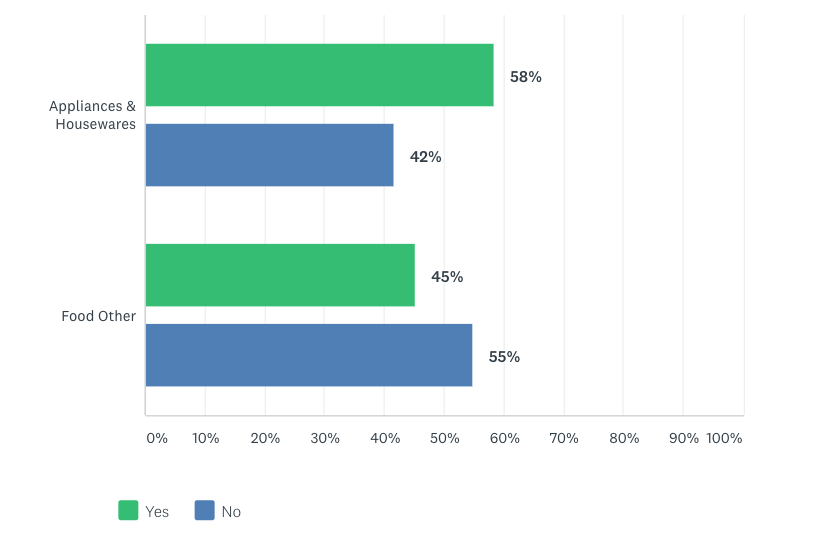

Perhaps the most significant impact in the appliance and housewares businesses is not the near-term impact on employee headcount, but a longer-term impact on company product roadmaps.

The graph below shows the results from where we asked our survey respondents whether they had to delay or cancel a product.

Figure 3: Has your company had to delay or cancel a new product due to COVID-19?

58% of those that worked for an appliance or housewares company indicated that their company had delayed or outright canceled a new product. This compares with 45% of those who worked in other food-related industries.

Why cancel or delay? The biggest reason for respondents was lower revenue/shrinking business, with over four in ten (43%) staying this was a reason. Another big reason (respondents were allowed to pick more than one contributing factor) was the impact of COVID on potential customers (40%), while another factor was COVID-related business disruption (38%).

Other reasons stated by at least two startups in the appliance space was lost funding rounds as investors grew skittish due to the impact of COVID-19.

The aggregate data tells a story of an appliance industry that has been hit hard, but differently than restaurants and other food-related businesses. How so? Perhaps more so than non-hardware businesses, appliances, and housewares companies often plan for revenue in the coming year or years with new products that, if canceled, will undoubtedly impact their outlook. New products often take years to bring to market, and the reality is the cancellation of a future product very likely changes the outlook of the company for years.

But it’s even bigger than that. New products often represent a company’s future vision for itself. Not to be too grandiose, but in some ways canceling a product is equivalent to a company canceling or delaying a vision of their future selves.

Not that these companies shouldn’t have shifted strategies. The reality is the landscape is going to be different. Consumers will have less money. The way they buy food and how they consume food is (and already has) changed. To not change how your company navigates a landscape where the map is suddenly much different would be a breach of your fiduciary duties as a company executive.

But it’s still worth trying to understand the long-term impacts of these many altered product roadmaps. To do that, it’s worth looking at what types of products were canceled or delayed.

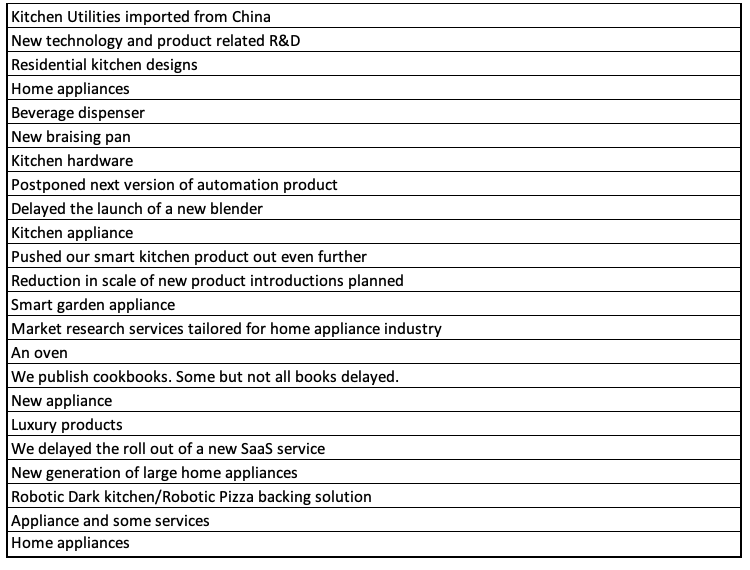

The table below shows some of the products listed by the respondents:

Table 1: What type of product or service did you delay or cancel due to COVID-19?

As you can see, many responses were fairly generic (“kitchen appliances” or “home appliances”). Others were more granular (“braising pan”, “beverage dispenser” or “smart garden appliance”). Others spoke to more services-related products related to the appliance or houseware industry (“SaaS service” or “Residential kitchen designs”).

But what is most telling, to me at least, is how the language speaks to how these companies are canceling what is next. One respondent said their company is canceling a “new generation of large home appliances”. Another “postponed next version of automation product .” A third cut “new technology and product-related R&D.”

Again, we’re traversing a new world. Product roadmap adjustments are required. But I can’t help but wonder how much innovative work and progress was lost due to COVID-19. In the coming weeks, I’ll continue to evaluate how the reshaped appliance industry landscape will look and what I expect kitchen tech and food-related innovation efforts will look like as we emerge on the other side.

Quick Thoughts

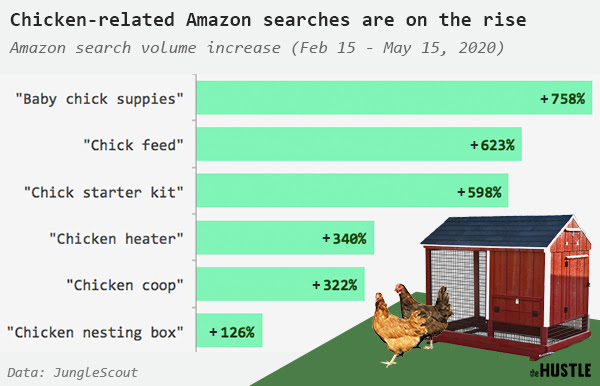

Chickens Are Hot

I wrote a couple weeks ago about how smart garden equipment was seeing a massive surge as consumers. In that post, I also mentioned that interest in backyard chicken farming was also on the rise, no doubt due to the same inclinations that led people to start buying seeds and developing plants for backyard gardens at a record rate over the past month or two.

But the sheer jump in interest in chicken-farming related products on Amazon is worth looking at. As show in the graphic below, Amazon-related searches for backyard chicken farming related products has most definitely shot through the roof. Chick supplies? Up eight-fold. Chick starter kit? Six-fold. Interest in chick coops has tripled.

I don’t think we’ll necessarily see tens of millions of chicken farmers, but I would definitely say the pandemic has meant chicken-farming has jumped the chasm from hipster hobby to a broader swath of the population concerned about their own food supply in what has been revealed to be, perhaps more so than they thought, a somewhat fragile food supply chain.

As I wrote last month, consumers are thinking about food sovereignty, many for the first time in their lives, and so I expect at-home food production to continue to be a big trend going forward.

Meal Kits 2.0?

It’s pretty easy to diagnose the reason for the demise of first-generation meal kits at this point: They were expensive and oftentimes required a lot of work for people who, at the end of the day, wanted to get food on the table at, yes, the end of the day.

But in some ways, I think the meal kit may be making a come back in products like that from Omsom, a meal-starter-by-mail service that allows you to essentially cook authentic Asian cuisine with little to no previous experience. In a way, it’s similar to the vision that ChefSteps had with their Joule-ready sauces, which I thought (and still do) think is a good idea before it became a victim of ChefSteps company-specific financial problems.

I also like Yo-Kai’s meal kit concept, even though it’s slightly different from Omsom in that the product provides the entire meal (including proteins). As you can guess by now, I love Asian food, and while I think Asian food meal kits probably are just better because Asian food is better (sorry not sorry), I think it’s more about not only being convenient and making life easier, but it’s also tapping into food passions. I’m going to be more passionate about an Asian food-by-mail offering than a more generic offering from the likes of Blue Apron or Plated. I also like the flexibility that greater and longer shelf-stability provides me (like with Omsom), which was always a problem with Blue Apron, which always felt like a race-against-the-clock for me.

ChefSteps has been working to diversify into food sales since 2014. Last year the company beta-tested a new line of business

ChefSteps has been working to diversify into food sales since 2014. Last year the company beta-tested a new line of business